Funding and Fiscal Implications

The issue of pensions, particularly the relevance of what is now called the (pre-2004) Old Pension Scheme (OPS) versus the New Pension Scheme (NPS), is now engaging the attention of all stakeholders. In the recent elections to the Gujarat and Himachal Pradesh Assemblies, a few Opposition parties took a stand to restore the OPS. The various stages of restoration of the old scheme in Punjab, Rajasthan, Chhattisgarh and Himachal Pradesh, have opened up a debate. This note attempts to analyse the issues in a dispassionate manner to enable us to take an informed view. The note has the following sections:

- Features of pension systems in India

- Perceptions of stakeholders

- Issues before the citizens and

- Fiscal implications of the pension system

a) The Features of the Pension System in India

The concept of a pension is generally understood as saving for the future from the present earnings for future requirements of oneself and the family. According to the Oxford Dictionary, it means “an amount of money paid regularly by a government or company to somebody who has retired from work.” A pension is broadly understood as a deferred compensation for their contribution while in service.

In India, all employees of Union and State Governments have been entitled to a pension as per the service conditions applicable at the time of joining government service. Pension schemes are also applicable to other organisations such as semi-governmental organisations, public sector banks, a few public sector undertakings, universities, and a few private companies as well. The pension system in India for government employees underwent a change on January 1, 2004, wherein the employees joining the service from the aforesaid cut-off date had to make a financial contribution towards a corpus for their pension to be received post-retirement. Before the introduction of the new system known as the National Pension Scheme (NPS), the fundamental difference between the pensions of government employees and others was that the government (both the Union and State) funded the burden of a pension while for all others the employees as well as the employer each made a contribution at a certain agreed ratio. All the government employees who had joined the service before 2004 would continue to be eligible to benefits from the OPS.

The pension includes half of the last drawn salary plus Dearness Allowance and the perks are not included while reckoning the last drawn salary. However, the pension undergoes a change whenever there is a revision of wages for serving employees, as also whenever there is Dearness Allowance paid by governments as per the extant policies. There is a provision for retiring employees to commute a certain fixed portion (about one-third) of the pension at the time of retirement wherein that amount, can be converted into cash by discounting the cash outflows over, say, a fifteen or twenty-year period. After the said period, the commuted portion will be restored to the pension thereby augmenting the pension drawn. There is also a concept of the Family Pension wherein the surviving spouse and, in some cases, the children, become entitled to a family pension of around two-thirds of the original pension. Additionally, the retirees under OPS have been provided with certain medical facilities, which include hospitalisation, provision of medicines, outpatient treatment, etc.

b) Perceptions of the Stakeholders

The stakeholders typically include the Union Government, State Governments, pensioners under the old and new schemes, employees in non-government sectors (who are not part of the pension schemes) and the public at large. Let us look at the issue through the respective prism of each stakeholder.

b.1) Union Government

The pension system in the Union Government was inherited from the colonial government. It started realising that such a system would be unviable fiscally in the context of the market economy. However, it took several years to follow the international best practices of fully funded pension schemes in line with market economies and in consonance with fiscal responsibility legislation. The challenge for the Government, going forward, is to continue servicing the OPS. The bigger challenge will be to provide adequate budgetary allocations, year after year, not only for the pension but also for the periodic increase in Dearness Allowance as also the updations consequential to the ongoing future wage settlements. The implementation of ‘One Rank One Pension (OROP)’ for the employees of Defence Services has opened up fresh demands from across the retiring and retired employees under OPS and such a consideration entails an additional increase in expenditure.

b.2) State Governments

The perception of the State Governments is by and large in sync with that of Union Governments. The NPS, which has been implemented across all the states and in the Union Government with effect from January 2004, was implemented by all states (except West Bengal) because of the obvious advantages associated with it. A few state governments, in reversal of the earlier stand, have decided to discontinue the NPS and bring back the OPS. However, a majority of the states are continuing with the NPS.

b.3) Individual pensioners under the old scheme

From the perspective of an individual, it is necessary to have social security and pension is nothing but a deferred wage compensation. It is legacy social security and should be continued with an ongoing improvement to ensure parity in compensation that is provided (or likely to be provided) to the government employees retiring prospectively. These pernsioners also opine that their contribution while they were in service has had an enormous beneficial impact on the nation going forward. They argue that in the absence of such a social security, government jobs will not attract people of talent and integrity.

b.4) Pensioners under NPS

Pensioners, i.e., employees who have joined the governmental service post January 2004, strongly feel that the relief envisaged under NPS is neither certain nor adequate and is subject to market vagaries since the corpus for the purpose is invested in bonds and equities. Even in the present dispensation, they desire that the contribution from the Government towards the corpus should be substantially enhanced while the contributions made by these employees deserve tax incentives. They overwhelmingly support restoration of the OPS.

b.5) Employees working in PSUs, Public Sector Banks, private sector, etc.

All the employees who are not entitled to pensions akin to those in the Government sector strongly feel that they are deprived of the requisite social security in the form of an assured pension. They also have a feeling that they have relatively tough working conditions, and their productivity is quantifiable. Employees working in PSUs feel that, since PSUs are subsidiaries of Government, there need parity with Government employees in the pension. Employees of Public Sector Banks feel that their pensions are meagre and adequate budgetary allocations are not being made by the banks and, hence, the scope for updation of pensions is diminishing.

c) The Issues Before Citizens

Citizens have a fundamental objection to just one section of citizens becoming eligible to deferred wages, which is discriminatory and biased. It is argued that the NPS is a rational approach wherein the employers’ contribution can be reckoned as deferred wages and the contribution of the employees can be considered as the traditional savings for building a pension for the rainy day. These contractual savings will also work in the national interest when deployed for capital formation. Since the NPS has been extended to every section of the organised work force, it can be portrayed as an equitable instrument of social security.

It is also argued that a pension only to certain sections amounts to discrimination between government and unorganised sectors. It is also opined that since under the OPS Governments are mandated to provide pensions from budgets, it pre-empts resources which otherwise should have gone for providing for basic needs such as health, education, nutrition, social infrastructure, etc., to the larger section of population.

d. Fiscal Implications

As per data available, the total number of Union Government pensioners and the total expenditure incurred during the financial year 2021-22 were 69,76,240 (69.7lLakhs) and Rs. 2,54,284 crore respectively1. The average annual pension per retiree for the year 2021-22 was Rs. 3,64,500. These pensioneers include retirees from all civilian, defence, telecom, railways and postal departments. With the shift to NPS from 2004, as per the NPS Trust, of the total registered subscribers of 1.67 crore, the total number of Union Government subscribers has reached 23.2 lakh , with a total contribution of Rs. 1.74 lakh crore. While the total number of pensioneers at the state level is not be readily available, the total number of State Govt. subscribers to NPS has reached 59.7 lakhs, with a contribution of nearly Rs. 3.24 lakh crore.

d.1) What is the Pension Payment Liability of the Government of India?

The total pension bill of the Government of India as per the 2022-23 budget estimates is Rs. 2,08,131.61 crore-constituting 10.72 per cent of the tax revenues of the Union Government and 9.4 per cent of the total (tax and non-tax) revenue of the Union Government. For the same year, as a per cent of revenue expenditure, pension bill is 6.5 per cent and as a percentage of revenue deficit, it is 21 per cent. These figures imply that around 1/5th of the borrowed resources of the Union Government are used for pension payments.

The pension burden has implications for intergenerational equity – an issue that needs careful discussion. The impact of the NPS is still not fully reflected in terms of the Union Government’s financial savings, as the OPS is still in operation for those who joined the service before April 1, 2004. Over time with the reduction in OPS commitment, the impact of pension expenditure on both the Union and State Government budgets should reduce. However, at the state level, in recent times, some states have decided to revert to the OPS, which can increase pension expenditure.

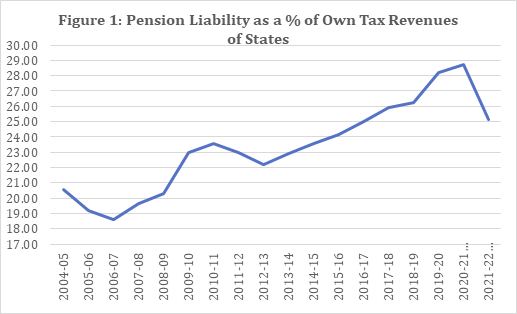

As evident from Figure 1, the pension liability, as a percentage of own tax revenue of the states increased from 20.54 per cent in 2004-05 to 28.74 per cent in 2020-21 (RE) even when the NPS was in operation. This burden was primarily due to the presence of large number of beneficiaries under the OPS.

This shift in policy raises the question whether the burden of pension liability will increase due to the reversal of NPS to OPS. If so, what is the implication of such an increase for the fiscal deficit, debt and intergenerational equity?

Intergenerational equity of any government expenditure programme is linked to the current level of deficit and debt that need to be serviced by future generations. The government of the day is in charge of managing taxation, expenditure and borrowing, and is responsible for the level of deficit, which gets added to the existing stock of debt. As mentioned earlier, the pension liability of the Union Government is more than 20 per cent of the revenue deficit. For 2022-23, States budgeted an increase in revenue spending, mainly led by non-developmental expenditure such as pension and administrative services2. The RBI Study on State Finances (2023) mentioned that

“(A) major risk looming large on the subnational fiscal horizon is the likely reversion to the old pension scheme by some States. The annual saving in fiscal resources that this move entails is short-lived. By postponing the current expenses to the future, States risk the accumulation of unfunded pension liabilities in the coming years.”

It is also to be noted that the pension liability of the states for the year 2022-23 (BE) is Rs 4,63,436.9 crore, which is 222.66 per cent higher than the expenditure on pension by the Union Government. Given that the combined debt of the Union and State Governments for the year 2022-23 (BE) is around 87 per cent of GDP, it is important to reflect on the fiscal implications of going back to the OPS at the state level.

The notion of intergenerational equity assumes far more importance in this scenario as the NPS was seen as a major reform in pension systems. As pensions in a defined benefit system are linked to indexation, revision and commutation, the fiscal burden of the pension would only be expected to rise. The intergenerational equity principle would require rebalancing current expenditure programmes and maintain a balance between availability of resources across generations.

In India, a substantial part of the population remains outside social protection or old age income support programmes, of which pensions are a major source. Within the pensions, a small proportion of government services (including the Union and States ) continue to consume a sizable share of revenue which is only increasing. Reversing to the OPS will leave a smaller fiscal space for competing demands of health, education, social protection and livelihood, and promote intergenerational inequity.

However, one cannot ignore the issue that a return on NPS investment is pro-cyclical in nature. The possibility of some index-based resources assured return on investment can help achieve the balance between need and availability of resources.

1. Central Government pensioners – Total numbers & Expenditure केन्द्र सरकार के पेंशनभोगियों की कुल संख्या | StaffNews