by Pinaki Chakraborty and Kaushik Bhadra

Introduction

The Reserve Bank of India (RBI) study on State Finance published on 11 December contains fiscal data for the years 2021-22 (actuals), 2022-23 (revised estimates) and 2023-24 (Budget Estimates). Major highlights of the RBI study are presented below:

- States’ consolidated gross fiscal deficit to gross state domestic product (GFD-GSDP) ratio declined from 4.1 per cent in 2020-21 to 2.8 per cent in 2021-22, led by a moderation in revenue expenditure, coupled with an increase in revenue collection.

- Some States have budgeted for fiscal deficits exceeding 4 per cent of GSDP in 2023-24 as against the all-India average of 3.1 per cent. They also have debt levels exceeding 35 per cent of GSDP as against the all-India average of 27.6 per cent.

- The strong growth in SGST has been instrumental in reducing the vertical fiscal imbalance between the Centre and the States in recent years.

- The support received from the Centre in the form of 50-year interest-free capex loans has helped in reducing States’ interest burden.

In this article, we analyse emerging fiscal issues and fiscal risks at the State level based on the data available from the RBI Study on State Finances-2023-24.

Own Resources and Union Transfers

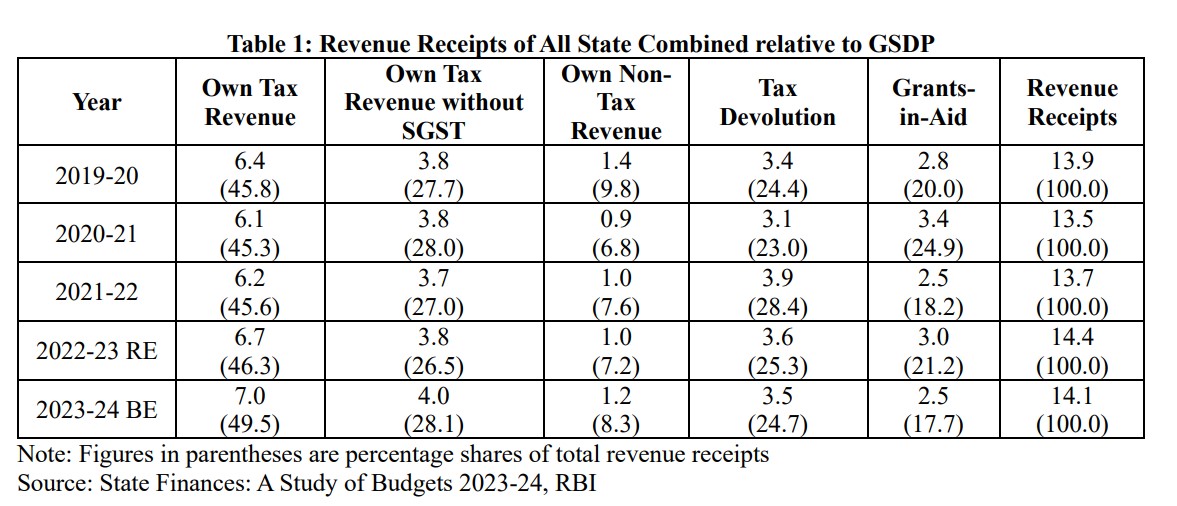

As evident from Table 1, between 2019-20 and 2023-24(BE), the own-tax revenue to GSDP ratio of States is expected to increase from 6.4% to 7.0%-an increase of 0.6 percentage points from its pre-pandemic level. However, non-GST revenue including taxes on petrol and diesel remained stagnant at around 4% of GSDP during this period. Both tax devolution and grants remained at around 6% of GSDP, except in the first year of the pandemic when the transfer of grants increased by 0.6 percentage points from its pre-pandemic level (2019-20). The share of grants declined from 20% of total revenues of the States in 2019-20 to 17% in 2023-24(BE). Transfer of grants as a % of GDP is expected to decline to 2.5% of GSDP in 2023-24(BE).

The increase in tax-to-GSDP ratio at the State level in India is similar to the tax revenue recovery at the Union government level. This is also similar to the revenue recovery at the global level after the pandemic. The Revenue statistics published by the OECD show that “the OECD average tax-to-GDP ratio rose by 0.6 percentage points (p.p.) in 2021, to 34.1%, the second-strongest year-on-year increase since 1990. The report also shows that tax-to-GDP ratios increased in 24 of the 36 OECD” countries after the pandemic.

Patterns of Expenditures

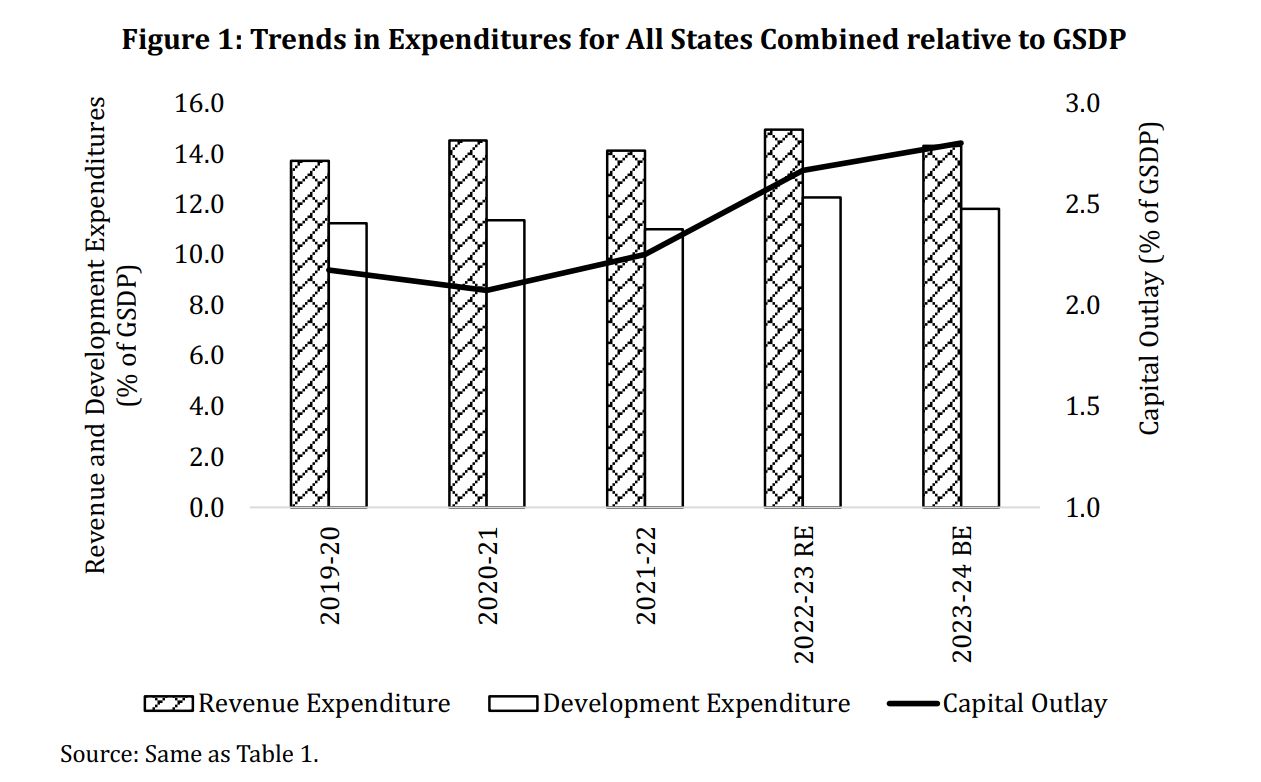

On the expenditure side, it is evident from Figure 1 that States’ aggregate revenue expenditure as a percentage of GSDP increased from 13.7% in 2019-20 to 14.5% in 2020-21. It is budgeted to decline to 14.3% in 2023-24 (BE). In contrast, the aggregate capital outlay to GSDP ratio has shown a gradual rise from 2.1% in 2020-21 to 2.8% in 2023-24 (BE). This increase in capital expenditure can also be attributed to the 50-year interest-free loans to the States given by the Union government on a year-on-year basis since the onset of pandemic. However, revenue deficit at the State level has also risen in recent past. In the context of rising revenue deficit at the State level, an increase in capital expenditure driven by interest-free loans from the Union is incentive incompatible. It has the potential to substitute capital expenditure financing by States from their own resources. Instead of providing interest free loan, a capital grant fund to the states linked to revenue deficit reduction may be considered as an alternative.

State Level Deficits

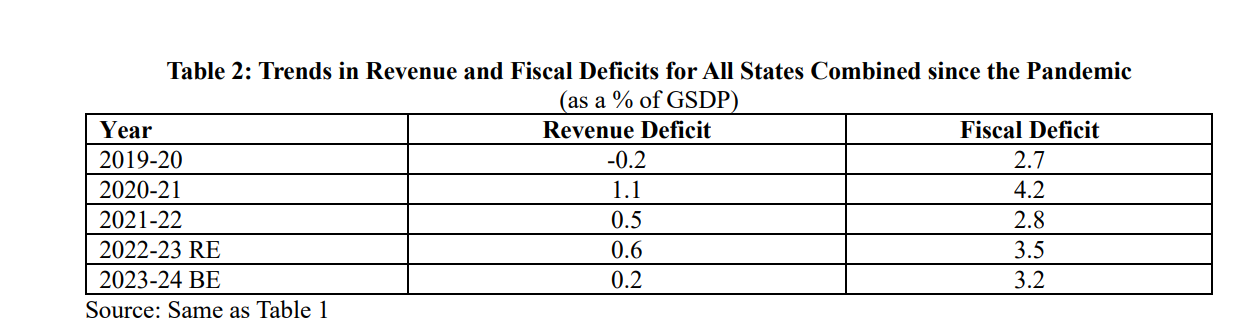

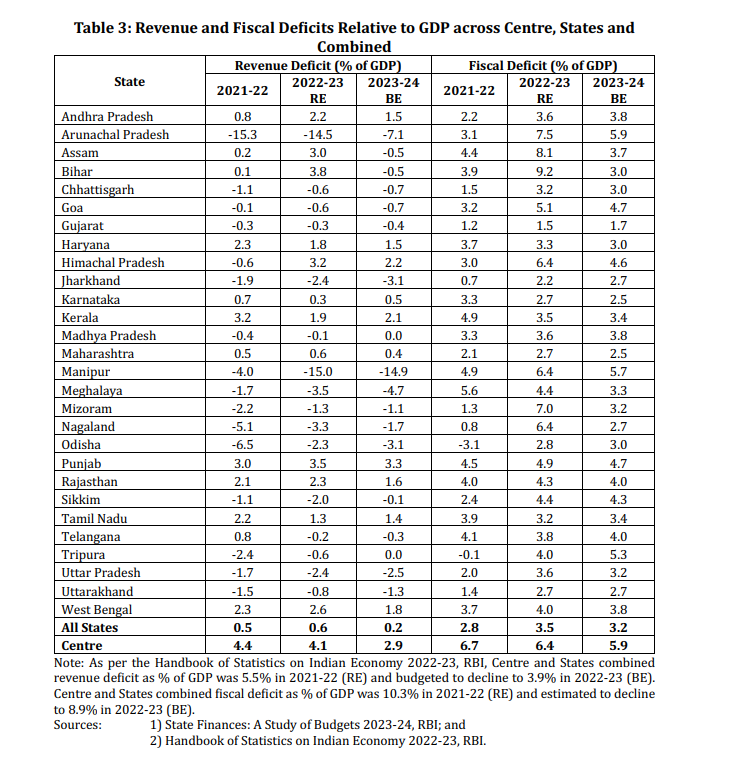

The all-State fiscal deficit increased from its pre-pandemic level of 2.7% in 2019-20 to 4.2% in 2020-21 (see Table 2). It declined to 2.8% in 2021-22. This ratio is estimated to increase to 3.5% in 2022-23 (RE) and budgeted to be 3.2% in 2023-24 (BE). Aggregate revenue account balance at the State level generated a surplus in 2019-20. However, the revenue surplus situation turned into revenue deficit in the year 2020-21 and is continuing. Among the major States, the level of revenue deficit in six States (Haryana, Kerala, Punjab, Rajasthan, Tamil Nadu and West Bengal) recorded a level much higher than the all-State average (See Table 3) during this period. For a comprehensive understanding of the general government fiscal deficit, the data on Union government deficits are also presented in Table 3. As evident from the Table, the revenue deficit of the Union government declined from its peak of 4.4% of GDP in 2021-22 to 2.9% in 2023-24 (BE). The fiscal deficit of the Union also declined from 6.7% to 5.9% during the same period.

Underutilisation of Fiscal Space

The borrowing limit of States was enhanced during the pandemic. This enhancement in borrowing limit had two objectives: a) to provide necessary resources to the States in the face of covid induced revenue contraction; and b) as a countercyclical expansionary fiscal measure to enable the States to make additional spending for post-pandemic economic recovery.

The 15th Finance Commission (FC-XV) recommended a revised fiscal roadmap from 2021-22 onwards considering the spillover effect of the pandemic. Consequently, the Union government, as per the recommendations made by the FC-XV, allowed the State governments to borrow an additional 1% of their GSDP by relaxing the fiscal deficit target under the Fiscal Responsibility and Budget Management Act from 3.0% to 4.0% in 2021-22 and 3.5% in the subsequent year. Besides, an additional borrowing of 0.5% of GSDP was also allowed to the States for a four-year period from 2021-22 to 2024-25. This additional borrowing was made conditional and linked to the power sector reforms at the State level.

It is evident from Figure 2, a large number of States underutilised their borrowing limits during the fiscal year 2021-22. States that borrowed over and above their borrowing limits were Assam, Kerala, Manipur, Meghalaya, Punjab and Telangana. Other than these six States, fiscal correction in the remaining States was more than the mandated borrowing limits for those years. Excessive fiscal corrections coupled with the emergence of revenue deficits resulted in a situation of underutilisation of fiscal space and lower capital expenditure than its potential at the State level.

Debt and Contingent Liabilities

The pre-Covid all-State debt to GSDP ratio for the year 2019-20 was 27.3%. This increased to 31.7% in 2020-21 and declined to 29.8% in 2021-22. Guarantees issued by the State governments usually constitute their contingent liabilities. If the guarantees are invoked, that could lead to a sudden increase in cash outflows and thereby increase deficit and debt. In this regard, the recent RBI Report of the Working Group on State Government Guarantees (2023) argued that upfront cash payment does not usually occur in the case of guarantees issued and this is one of the prime reasons behind the increase in guarantee at the State level. However, literature shows that ambiguity regarding the timing and quantum of potential cash outflows against the issued guarantees makes fiscal management intricate for the subnational governments and bears enormous implications on the stock-flow adjustments of debt and deficit (Campos et al., 2006). An increase in guarantees extended by the State governments during the period 2019-20 to 2021-22 is evident from Table 4.

A number of studies found that contingent liabilities impact the debt spike more than fiscal deficit (Campos et al., 2006) and off-budget operations have become a reliant path to circumvent the fiscal rules (von Hagen and Wolff, 2006). Contingent liabilities in advanced and developing economies have not only driven debt spikes but also have been considered as major deterrents for fiscal transparency (Jaramillo et al., 2017). International evidence also suggests that fiscal rules have induced governments to use off-budget operations as a form of creative accounting (Milesi-Ferretti, 2003). Since fiscal risks due to off-budget operations show an increase at the State level in India, it is important to improve fiscal transparency regarding off-budget operations. Strengthening institutional mechanisms to monitor off-budget borrowing at all levels of government would reduce fiscal risk emanating and impart greater stability to the budgetary operation.

Power Sector DSICOM Finances and Fiscal Risks

Finally, the risk emanating from the financing of DISCOM remains a major source of fiscal risks for the State governments. The RBI Study on State Finances-2023-24 observed that “Power distribution has strained State finances due to persistent operational inefficiencies and significant under-recoveries. Receipts from the power sector constitute less than a tenth of the corresponding revenue expenditure incurred by the States.” The major issues in the context of DISCOM finances highlighted are low tariff rates, high procurement costs of power, cross-subsidisation, and the dominance of State authorities which limits decision-making autonomy. A recent study by Josey A et al (2024) observed that “The aggregate annual losses of State-owned DISCOMs are comparable to 35% of the aggregate revenue deficit of State budgets in 2021–22”. The study further noted that “ There is wide variation in the extent of losses across States but the fact remains that if State governments were to take over annual losses, the impact on State finances would be significant.”

Conclusions

To conclude, fiscal situation has improved at the State level after the pandemic. However, multiple fiscal risks remain and some of these risks are also increasing due to the off-budget operations of the States. However, the debt and deficit profile and consequent fiscal risk vary across States. These State specific fiscal vulnerabilities need appropriate policy considerations to enable sustainable fiscal recovery,.

Pinaki Chakraborty is currently the Vice Chairman, Institute of Development Studies, Jaipur and Kaushik Bhadra is an independent public finance management consultant and former consultant to the Haryana State Finance Commission.

References

Campos, C.F.S., Jaimovich, D., & Panizza, U. (2006). The unexplained part of public debt. Emerging Markets Review, 7(3): 228-243.

Jaramillo, L., Mulas-Granados, C., & Kimani, E. (2017). Debt spikes and stock flow adjustments: Emerging economies in perspective. Journal of Economics and Business, 94: 1–14.

Josey, A., Dixit, S., Sreekumar N., and Jog, M (2024). Indian Electricity Distribution Companies amidst Churn: Understanding Present Challenges and Shaping Future Opportunities, https://forumforstatestudies.in/wp-content/uploads/2024/03/DISCOM-Finance-Article_Prayas_120224.pdf

Milesi-Ferretti, G. (2003): Good, Bad or Ugly? On the Effects of Fiscal Rules with Creative Accounting. Journal of Public Economics, 88: 377–394.

RBI (2023). Report of the Working Group on State Government Guarantees, Reserve Bank of India, Mumbai.

RBI (2023): State Finances: A Study of Budgets of 2023-24, Reserve Bank of India, Mumbai.

Von Hagen, J., & Wolff, G. B. (2006). What do deficits tell us about debt? Empirical evidence on creative accounting with fiscal rules in the EU. Journal of Banking and Finance, 30(12): 3259–3279.